Transport tax declaration sample to fill out. Consequences for violating the deadline. How to fill out a transport tax return - Cover page

For 2017 reporting, transport tax returns must be submitted on new forms. A new declaration form approved by order of the Federal Tax Service of Russia dated December 5, 2016 No. ММВ-7-21/668.

Let us explain in the table what has changed in it:

| Declaration indicators | New form | Old form |

|---|---|---|

| Front page | There is no print field | There is a printable field |

| Section 2 “Calculation of the tax amount for each vehicle” | Added lines: – 070 – vehicle registration date; – 080 – date of termination of registration of the vehicle (deregistration); – 130 – year of manufacture of the vehicle. | In the previous form there were no such lines |

| Lines have appeared for deductions that are used by payers of contributions to the Platon system (owners of vehicles weighing over 12 tons). Line 280 shows the deduction code, and line 290 shows the deduction amount. |

What are the deadlines for submitting the transport declaration for 2017?

Article 363.1 of the Tax Code of the Russian Federation regulates the deadlines for submitting transport tax declarations. Organizations submit reports on vehicles once a year. The deadline is February 1 of the following year. If the last day of the deadline falls on a weekend, it is shifted to the next working day (Clause 7, Article 6.1 of the Tax Code of the Russian Federation). However, since February 1 fell on a Thursday in 2018, the dates are not postponed. The declaration must be submitted to the Federal Tax Service no later than February 1, 2018.

Please note that the specified deadline for submitting a transport tax return is the same for all companies. There are no special rules or exceptions regarding when a transport tax return is submitted in the Tax Code of the Russian Federation. It is very convenient that the procedure for filling out a tax return for transport tax allows companies to choose how to submit it:

- personally or through a representative;

- by mail with a description of the attachment or by sending an electronic report.

If you choose postal services, the declaration is considered submitted on the day the postal item is sent. And when transmitted via TKS - the date the file was sent.

Submit your transport tax declaration to the same inspectorate where you pay the tax. That is, according to the location of vehicles (clause 1 of article 363, clause 1 of article 363.1 of the Tax Code of the Russian Federation).

Who exactly should report for 2017 in 2018

Legal entities (Article 363.1 of the Tax Code of the Russian Federation) on which vehicles are registered (Article 357 of the Tax Code of the Russian Federation) are required to submit a transport tax return for 2017. And not just any, but those that are recognized as taxable: cars, motorcycles, buses, yachts, boats, motor boats, etc. (see Article 358 of the Tax Code of the Russian Federation).

The same article provides a list of items whose registered rights do not oblige you to fill out a transport declaration for 2017, since these are not taxable items. For example, a stolen car or agricultural transport.

Should “physicists” report?

Unlike legal entities, a tax return for transport tax by individuals is not filled out and submitted (Clause 1, Article 362 of the Tax Code of the Russian Federation). Tax authorities themselves will calculate this tax to be paid based on data from the traffic police. Thus, for ordinary citizens, a transport tax declaration for individuals is replaced by a notification from the Federal Tax Service for the payment of transport tax. There is no need to download the transport tax return. By the way, you can check whether the inspectorate calculated the transport tax correctly using a special service on the official website of the Federal Tax Service. Exact link.

As for individual entrepreneurs, they are fully subject to the rules of reporting and payment of transport tax that apply to ordinary individuals. Even if the merchant uses the vehicle to make a profit. Thus, individual entrepreneurs do not submit a transport tax return for 2017, but pay the tax based on a notification from the Federal Tax Service.

Composition of the new transport declaration in 2018

The new transport tax return for 2017 for legal entities consists of a title page and two sections.

As we have already said, in the second section of the declaration for 2017. in which the tax amount for each vehicle is indicated, five lines appeared:

- in lines 070 and 080 you can now indicate when the vehicle was registered (with the State Traffic Inspectorate, Gostekhnadzor, etc.) and when it was deregistered;

- on line 130 – year of manufacture;

- lines 280 and 290 - code and deduction amount are filled in by payers of fees in the Platon system (owners of vehicles weighing over 12 tons).

Data about the car - identification number (VIN), make, registration number, registration date, year of manufacture, take from the title or registration certificate. Indicate the registration termination date (line 080) only for cars that you deregistered in the reporting year.

Filling out a new declaration form: examples and samples

Title page of the declaration

On the title page, indicate basic information about the organization and the declaration.

TIN and checkpoint

Please include these codes at the top of the title. If you are reporting on the location of a separate unit, indicate its checkpoint.

Correction number

Please indicate here:

- if you are submitting a report for the first time – “0–”;

- if you are specifying something that has already been submitted, the serial number of the report with corrections (“1–”, “2–”, etc.).

Tax period

Enter code “34” in your transport tax return.

Reporting year

In this case, 2017 is the year for which reporting is submitted.

- In the “Submitted to the tax authority” field, enter the Federal Tax Service code;

- in the line “at the location (registration) (code)” put 260 if you are submitting a declaration at the place of registration of the organization, division, or vehicles. Code 213 means the largest taxpayers, and code 216 their legal successors.

Taxpayer

Here record the full name of the organization in accordance with the constituent documents.

OKVED

In this field, enter the code according to the All-Russian Classifier of Types of Economic Activities (OKVED) OK 029-2014 (NACE revision 2).

Section 1 of the declaration

After completing the title page, skip Section 1 and begin completing Section 2. Based on the information in this section, then complete Section 1.

Line 120

Fill out line 120 only if the tax rate depends on the number of years from the year of manufacture of the car.

Line 140 and 160

In line 140, indicate the number of full months of car ownership during the year, and in line 160 - the coefficient Kv. If you owned the car all year, put 12 in line 140, and 1 in line 160.

Enter the number of months of 2017 during which your organization owns a specific vehicle in line 140. Please note that full months include those in which the vehicle was registered before the 15th day (inclusive) and deregistered after the 15th day. Months in which the vehicle was owned for less than half a month are not taken into account. Divide the number of complete months of vehicle ownership by 12 to obtain the ownership coefficient, which is reported on line 160. This coefficient is rounded to four decimal places.

Line 150

In line 150, put 1/1 if the owner is the only one. Otherwise, it is indicated as a fraction (1/2, 1/3, etc.).

Line 180

Indicate the Kp coefficient (line 180) only for expensive cars.

Lines 190 and 300

In lines 190 and 300, indicate the calculated tax for the year.

Enter the amount of calculated tax on line 190. To do this, calculate it using the formula:

For vehicles that are completely exempt from tax, put a dash in line 300.

Lines 200 – 290

These lines are filled in by “beneficiaries”. Subjects of the Russian Federation have the right to exempt an organization from transport tax or reduce it for some vehicles. In this case, fill out lines 200-270.

When a vehicle falls under the benefit, line 200 indicates the number of full months of use of the benefit in 2017. To calculate the coefficient of use of the Kl benefit (line 210), the data on line 200 is divided by 12 months. The coefficient is rounded to four decimal places. The type of benefit and amount are deciphered in the lines:

- 220-230 – complete tax exemption;

- 240–250 – reduction of the tax amount;

- 260–270 – reduced tax rate.

If vehicle benefits are not established, dashes are placed in lines 220–270.

Section 1 of the declaration

By filling out section 2 for all vehicles, go to section. 1.

If you do not pay advance payments, in lines 021 and 030, indicate the total tax amount for all cars.

If you pay, indicate advance payments in lines 023 - 027, and in line 030 - tax payable at the end of the year.

The car has an engine power of 105 hp. With. was sold and deregistered on December 13, 2017. The car was produced in 2015 and registered on 10/21/2015. In the region there are advance payments, the tax rate is 35 rubles/l. With.

- During the year, the organization owned the car for 11 months from January to November.

- Advance payments for the 1st, 2nd and 3rd quarters – 919 rubles each. (1/4 x 105 hp x 35 RUR/hp).

- The coefficient Kv for calculating tax for the year is 0.9167 (11 months / 12 months).

- The calculated tax amount for 2017 is RUB 3,369. (105 hp x 35 rub/hp x 0.9167).

- The amount of tax payable for the year is 612 rubles. (3,369 rubles – 919 rubles – 919 rubles – 919 rubles).

New form "Tax return for transport tax" officially approved by document Appendix No. 1 to the order of the Federal Tax Service of Russia dated December 5, 2016 No. ММВ-7-21/668@.

More information about using the form "Tax return for transport tax":

- Do I need to pay transport tax and property tax on a car trailer?

The organization is not required to pay transport tax and include the trailer in question in the transport tax return. 2... . In the Moscow region, the tax rate is..., there is no need to pay transport tax on a car trailer. The Organization is required to submit a transport tax return to the tax authority...

- Exemption of agricultural transport from transport tax

The tax authority at the location of the vehicles, unless otherwise provided by this article, a tax return for transport tax... . Taxpayers who are organizations and pay advance tax payments during the tax period..., nor in the Procedure for filling out a transport tax return (hereinafter referred to as... control ratios of the indicators of the transport tax return form, sent by a Letter from the Federal Tax Service...

- On submitting an updated income tax return

Submits updated tax returns for this OP to the tax authority at the location... 264 of the Tax Code of the Russian Federation (transport tax, property tax, land tax, insurance premiums). For example... from a taxpayer submitting an updated tax return for the specified tax (see Letter from the Federal Tax Service... an excessively calculated amount of land, transport taxes, property taxes, insurance premiums... a tax return, the results of which did not establish the fact of a violation of the law about taxes...

- Penalties for violating the deadline for submitting declarations and settlements. Accounting and tax accounting

G. - 01/25/2018 Income tax Tax return for income tax If the reporting... 2017 - 03/30/2018 Transport tax Tax return for transport tax For 2016 - 02/01... - 02/01/2018 Land tax Tax return for land tax For 2016 - 01 ... Tax return for the simplified tax system Declaration for UTII Declaration for the Unified Agricultural Tax Declaration for property tax for the year Declaration for transport tax Declaration for land tax Help for...

- Let's talk about transport tax

Are there additional charges for transport tax (up to the annual amount) made by the inspection based on the results of the “camera” tax return for... for transport tax (up to the annual amount) made by the inspectorate based on the results of the “camera” tax return for 2015? Transport tax... for a car - seven months. Based on the results of a desk audit of the transport tax declaration for 2015, the inspectorate... assessed additional tax to the annual...

- For 2018, you need to report on land tax in a new way

Once, despite the fact that the form of the land tax declaration (hereinafter - the Declaration) and its procedure... once, despite the fact that the form of the land tax declaration (hereinafter - the Declaration) and its procedure... the tax period for the land tax is a calendar year. At the end of the tax period, taxpayers-organizations submit a Declaration... to zones and zones of engineering and transport infrastructures. Land plots assigned... to zones and zones of engineering and transport infrastructures 003002000110 – Land plots...

- New in the legislation on taxes and insurance premiums

Including machinery, equipment, machine tools, vehicles, equipment for production, storage... The Tax Code of the Russian Federation has updated the tax return and tax calculation for the advance payment of property tax... land tax, you will have to submit a tax return for 2018 to the tax office authority on... 21/509@. The current version of the land tax return is presented starting with the report... The need to make changes to the land tax return is associated with bringing it into...

- Features of accounting for tax obligations

Obligations (payments) Monetary obligations to pay taxes Tax returns, calculations Date of acceptance of the obligation Amount... accrued obligations (payments) Accounting for tax calculations... art. 359 of the Tax Code of the Russian Federation). Tax rates for transport tax are established by the laws of the constituent entities of the Russian Federation in... tax liability at the end of the reporting year, despite the fact that the tax return will be...

- What to do if your VAT return has not been accepted?

In the amount of 5% of the amount of tax payable, but not... be more than 30% of the tax payable and less than 1... assessment of the legality of the actions of the tax authority.” Example. The company sent a VAT tax return to... a notice of refusal to accept a tax return on the grounds: “the declaration contains errors and does not contain... attachments, the transport container was not installed; evidence of non-compliance of the submitted declaration with the established... transactions, the share of deductions in the amount of tax calculated on taxable transactions,...

- The procedure for drawing up, composition and deadlines for submitting annual reports according to the simplified tax system for 2015. Form and procedure for filling out the declaration. Example

She must submit tax reports: - tax return for a single tax; - tax returns for transport and land taxes, if recognized... as a payer of these taxes; - information about... she must submit tax reporting: - tax return for a single tax; - tax returns for transport and land taxes, if recognized...

- Review of Federal Tax Service Letters and tax changes for the second quarter

The question of amending the tax return for land tax, providing for the possibility of using two... filling out a tax return for corporate income tax" The Federal Tax Service of the Russian Federation explained the procedure for reflecting in the tax return for tax... a tax return for value added tax" Federal Tax Service of the Russian Federation reports codes to be reflected in the tax return for... what if, at the time of sale of a vehicle used in business activities...

- Assorted questions on property taxes

Premises and parts of buildings or structures intended to accommodate vehicles... are of interest to property tax payers. New land tax declaration Starting with reporting... year, land tax payers must submit a declaration to the tax authority in the form approved by the Order...: control ratios for the new land tax declaration are given in the Letter of the Federal Tax Service of Russia...

- Reflection in expenses of the amounts of transport tax and fees in the Platon system

Understand the taxes and fees payable to the budget, reflected in the relevant declarations... the tax base at the end of the reporting periods is made based on the amount of advance payments for transport tax... t). Quarterly calculated advance payments for transport tax amount to 9,000 rubles. ... taxation, the amount of advance payment for transport tax is recognized - 9,000 rubles. plus... taxation, the amount of advance payments for transport tax is recognized - 18,000 rubles. plus...

- Long-term production: determining the tax base for VAT

Parts, including for vehicles; weapons and ammunition; radio... in the general manner.) If, according to the declaration, tax is expected to be paid, transfers to the budget... will not be able to adjust the calculated tax by submitting an updated declaration, as reported by the Federal Tax Service... VAT is taken into account in section. 3 VAT returns. The conclusion of the Ministry of Industry and Trade on the duration... The Federal Tax Service on the accrual of penalties on the company for the invalid tax and obliged the tax authorities to return...

- What main activities should an accountant take at the end of the year?

3/572. According to the new form, it is also necessary to submit a tax return for personal income tax... . Taxpayers submit a tax return using the current form. For the first time, taxpayers will have to report using the new declaration form... 2017. The tax authorities have prepared draft amendments to the VAT tax return in the form approved... they have also prepared draft amendments to the transport tax declaration, the form of which was approved by order...

In 2019, the deadlines for submitting a transport tax return remained the same, but the format of the document itself has changed somewhat. Read in this article what the new transport tax return for legal entities looks like, how to fill it out correctly, and also what deadline it needs to be submitted.

Deadline for submitting a transport tax return in 2019

Legal entities are obliged provide a transport tax return to the tax authority:

- by place of registration (for taxpayers classified as the largest);

- at the location of the vehicle (for all others).

Clause 1 Art. 363.1 Tax Code of the Russian Federation:

At the end of the tax period, taxpayers-organizations submit a tax return to the tax authority at the location of the vehicles.

Clause 4 art. 363.1 Tax Code of the Russian Federation:

Taxpayers, in accordance with Article 83 of this Code, classified as the largest taxpayers, submit tax returns to the tax authority at the place of registration as the largest taxpayers.

The document is sent no later than February 1 of the year following the completed tax period. According to clause 1 art. 360 Tax Code of the Russian Federation The tax period for transport tax is 1 calendar year. Therefore, the deadline for submitting transport tax for legal entities, for example, for 2017 is before February 1, 2018.

Clause 3 art. 363.1 Tax Code of the Russian Federation:

Tax returns are submitted by taxpayer organizations no later than February 1 of the year following the expired tax period.

Please note: If February 1st falls on a weekend, the deadline for submitting the declaration is postponed to the next business day.

Clause 7 art. 6.1 Tax Code of the Russian Federation:

In cases where the last day of the period falls on a day recognized in accordance with the legislation of the Russian Federation as a weekend and (or) a non-working holiday, the end of the period is considered to be the next working day following it.

The procedure for submitting the declaration and its structure

According to clause 2.6 of the Order of the Federal Tax Service of Russia dated December 5, 2016 N ММВ-7-21/668@ You can send the document to the tax office:

- personally or through a representative;

- by mail (with a description of the attachment);

- via the Internet (in the order specified in Order of the Ministry of Taxes and Taxes of the Russian Federation dated April 2, 2002 N BG-3-32/169).

Please note! If documents are sent by mail or via the Internet, the day of submission is considered the day of sending.

The transport tax declaration consists of 3 parts:

- Front page.

- Section 1(to be paid to the budget).

- Section 2(Calculation of the tax amount for each vehicle).

Detailed instructions for filling out each part of the document, taking into account changes, are described in Order of the Federal Tax Service of Russia dated December 5, 2016 N ММВ-7-21/668@. Below we will outline the main points that need to be taken into account when filling out the declaration, and also describe what needs to be indicated on each page.

Please note: Declarations for 2019 must be submitted using a new form. What is the difference between the old and new document format, read below.

General rules for filling out a tax return

When filing a transport tax return, adhere to the following rules:

- fill out the document blue, purple or black ink;

- use only printed capital letters;

- fixes and bugs unacceptable;

- if you submit a declaration in paper form, print each page on a separate sheet. Do not staple sheets using products that damage the paper;

- indicate calculations in full rubles. Values less than 50 kopecks not indicated, 50 and more - rounded to the nearest ruble;

- each cell should contain only one character;

- all cells of the field where any indicator is missing must contain a dash. A dash is also placed if there are extra cells left in the field.

Organizations that own vehicles must annually report transport tax to the Federal Tax Service at the place of registration of the vehicle (clause 1 of Article 363.1 of the Tax Code of the Russian Federation). An exception is provided only for car owners who are not subject to taxation and specified in paragraph 2 of Art. 358 Tax Code of the Russian Federation.

The largest taxpayers - owners of vehicles - submit a tax return for transport tax to the Federal Tax Service at the place of registration as the largest taxpayer (clause 4 of Article 363.1 of the Tax Code of the Russian Federation).

Cancellation of transport tax declaration

The Tax Service has prepared a bill according to which legal entities will no longer have to submit a transport tax return, as well as a land tax return. Organizations, as before, will pay transport and land taxes to the budget, and inspectors, for their part, will compare the amount paid with the calculated amount.

The abolition of transport and land tax declarations will undoubtedly make life easier for accountants.

The consent of Russian President Vladimir Vladimirovich Putin to cancel these declarations has already been received. It remains to wait for the corresponding amendments to be made to the Tax Code of the Russian Federation.

Deadline for submitting transport tax returns

The tax return for transport tax is submitted to the tax authority no later than February 1 of the following year (clause 3 of Article 363.1 of the Tax Code of the Russian Federation).

If the last day for submitting reports coincides with a weekend or holiday, then the deadline is postponed to the next working day (Clause 7, Article 6.1 of the Tax Code of the Russian Federation).

Based on the results of 2018, a tax return for transport tax must be submitted without a fine from inspectors no later than February 1, 2019.

According to the norms of the current legislation of the Russian Federation, the declaration of advance payments for transport tax is not submitted (clause 47 of article 2 of the Law of July 27, 2010 No. 229-FZ).

Transport tax declaration (form)

The tax return for transport tax (form), as well as the procedure for filling it out, have been approved No. ММВ-7-21/668@.

Procedure for calculating transport tax and payment deadline

The amount of transport tax for the year is determined as the product of the tax rate and the engine power (jet engine thrust, gross tonnage) of the vehicle (clause 2 of article 362, clause 1 of article 359 of the Tax Code of the Russian Federation).

Transport tax rates, deadlines for tax payment and advance payments on it are established in each region separately (clause 1 of Article 361, clause 6 of Article 362, clause 1 of Article 363 of the Tax Code of the Russian Federation). In this case, the deadline for paying tax for the year should not be set earlier than February 1 of the next year (clause 1 of Article 363 of the Tax Code of the Russian Federation).

For example, vehicle owners registered in Moscow pay tax only at the end of the year; advance tax payments do not need to be calculated and paid (Moscow Law No. 33 dated 07/09/2008). So, in Moscow, companies need to pay transport tax to the budget no later than February 5 of the next year (Clause 1, Article 3 of Moscow Law No. 33 dated 07/09/2008).

Algorithm for calculating transport tax for legal entities.

The procedure for filling out a tax return for transport tax

How to fill out a transport tax return - Cover page

The title page of the tax return indicates information about the organization (name, tax identification number, checkpoint, code of economic activity, telephone number), as well as the reporting year for which the report is submitted, and the code of the Federal Tax Service for which the declaration is submitted.

If the report is submitted for the first time in a year, the adjustment number will be “0”; when submitting an updated declaration, the adjustment number will be “1”, “2”, etc.

When submitting a return for the year, the tax period will be “34”; when submitting a return for the last period during the liquidation or reorganization of a company, the tax period will be “50”.

The tax authority code corresponds to the first four digits of the company's TIN.

When submitting a declaration at the location of a company or vehicle, code “260” is entered; if the declaration is submitted by the largest organization, then the code will be “213”; legal successors will enter code “216”.

The procedure for filling out a transport tax return - Section 1. The amount of tax to be paid to the budget

Section 1 of the tax return for transport tax indicates the budget classification code for transport tax, the territorial OKTMO code and the calculated amounts of the annual tax and advance payments, as well as the amount of tax that must be paid to the budget at the end of the year.

Filling out a transport tax return - Section 2. Calculation of the tax amount for each vehicle

In Section 2 of the tax return for transport tax, the amount of annual tax is calculated for each vehicle, indicating the territorial OKTMO code.

The vehicle type code is indicated on the basis of Appendix 5 to the Procedure by Order of the Federal Tax Service of Russia dated December 5, 2016 No. ММВ-7-21/668. For example, for a passenger car you need to enter the code “51000”.

The identification number, make, registration plate, registration date and year of manufacture of the vehicle are indicated in the state registration certificate.

The unit of measurement of the tax base is indicated in accordance with Appendix 6 to the Procedure for filling out the declaration, approved by Order of the Federal Tax Service of Russia dated December 5, 2016 No. ММВ-7-21/668. For example, the unit of engine power in horsepower is “251”.

The economic class and the number of years that have passed since the year of manufacture of the vehicle are filled out only by those organizations whose tax rate depends on these indicators (clause 3 of Article 361 of the Tax Code of the Russian Federation).

The number of full years of ownership of a vehicle is determined as follows: if the vehicle is registered before the 15th day of the month inclusive, then this month is equal to a full month of ownership, and also months in which the vehicle is deregistered after the 15th on the 2nd day (clause 3 of Article 362 of the Tax Code of the Russian Federation).

If there is only one owner of the vehicle, then when filling out the taxpayer’s share in the title to the vehicle, “1/1” is indicated; if there are several vehicle owners, then the share is indicated in accordance with the number of owners “1/2”, “1/3”.

To determine the ownership rate (line 160), you need to divide the number of months you own the vehicle by the total number of months in the year. For example, if you have owned a vehicle for 9 months, the ownership coefficient will be 0.75 (9: 12).

The increasing coefficient (line 180) is filled in only for expensive vehicles (clause 2 of Article 362 of the Tax Code of the Russian Federation).

Regional authorities may establish benefits that exempt from payment of transport tax in whole or in part.

Tax return for transport tax 2018

Transport tax return for 2018 - are there any differences in filling out compared to last year? Which form is used to prepare the 2018 return? How to fill lines 280 and 290? What are lines 070 and 080 for? The answers to these questions, as well as an example of filling out the declaration, are in this article.

Table of new lines in the transport tax return for 2017-2018

The transport tax declaration form was approved by order of the Ministry of Finance of Russia dated December 5, 2016 No. ММВ-7-21/668@. It is used to submit a transport tax return for 2018. For 2017, we reported on the same form - no changes were made to it.

It differs from the declaration of previous years by the presence of new lines in the structure:

When filling out the transport tax return for 2017-2018, please note that it contains:

- the entry of data is not confirmed by the company seal;

- the total amount of tax is reflected for all vehicles, the location of which is the territory of a constituent entity of the Russian Federation (by agreement with the tax authorities, received before the start of the tax period for transport tax);

- The tax is calculated taking into account the date of registration of the vehicle (before or after the 15th of the corresponding month).

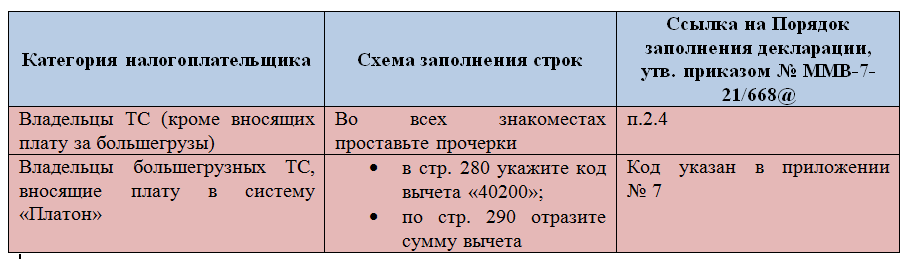

Technology for filling lines 280 and 290

The indicated lines of the transport tax declaration for 2017-2018 have two filling schemes:

Subscribe to our accounting channel Yandex.Zen

If you reflected numerical values in lines 280 and 290 (in 2017-2018 you paid for heavy vehicles), then in this regard, pay attention to filling out the declaration lines associated with them and other important nuances:

- in lines 023, 025 and 027, enter “0” (clause 4.5 of the Procedure, approved by order No. ММВ-7-21/668@);

- reduce the transport tax on payments for heavy vehicles if you paid the fee yourself and pay the tax yourself;

- reduce the calculated tax by the deduction reflected in line 290.

Before issuing a payment order for tax remittance, check the ratios:

- if TN ≤ NV → TN upl = 0 - do not issue a payment order;

This means that at the end of the year you do not have the obligation to pay transport tax (TN), if its amount is less than the tax deduction (TD) - the tax payable (TN deduction) is assumed to be equal to 0.

- if TN > NV → TN upl = (TN - NV) - transfer this amount to the budget.

When making a payment, do not forget to check the KBK for transport tax.

The tax on the specified deduction can be reduced only for those heavy-duty vehicles for which payments have been made to the system. The deduction does not apply to tax on other vehicles.

Purpose of lines 070 and 080

Using this information, tax authorities will be able to check whether you are correct:

- calculated the number of full months of vehicle ownership;

- took into account the “15th” rule.

This rule is described in paragraph 3 of Art. 362 of the Tax Code of the Russian Federation and is associated with the calculation of the vehicle ownership coefficient.

Find out from our publications whether you need to pay tax if you owned a vehicle:

- 1 day ;

- less than a month .

An example of filling out a transport tax return for 2018

Let's look at how to fill out a transport tax return, provided that two vehicles are listed on the balance sheet of Fantasia LLC (TIN 5017123456, KPP 501701001):

- Audi A6 Avant quattro passenger car (identification number УTH330700M1415145, registration plate - С285МА98, engine power - 249 hp, manufactured in 2017). Purchased on 08/27/2018.

- A truck with a carrying capacity of more than 12 tons (identification number XTU646008E2441447, brand - KamAZ-6460, registration plate - T182UE50, with an engine power of 400 hp, manufactured in 2011). The car was purchased on July 1, 2016. Registered in the Platon system. In 2018, the fee for compensation for damage to roads is 13,200 rubles.

Fantasia LLC operates in the Moscow region and is the sole owner of both vehicles.

The transport tax rate in 2018 in the Moscow region is:

- 150 rub. for 1 l. With. for the Audi A6 Avant quattro;

- 85 rub. for 1 l. With. for the KamAZ-6460 vehicle.

You can check what transport tax rates are established in your region in the article “Transport tax rates by region - table 2018-2019”.

The Audi A6 Avant quattro is included in the list of expensive cars; an increasing factor of 1.1 is applied in the calculation.

What to do if the car is expensive, but it is not on the list of the Ministry of Industry and Trade, see.

The annual amount of transport tax is:

- for the Audi A6 Avant quattro:

249 l. With. × 150 rub./l. With. × 1.1 × 0.3333 = 13,694 rubles,

1.1 is an increasing factor for expensive cars;

0.3333 is the ownership ratio, defined as the number of complete months of ownership (4 months) divided by the number of months in a year (12).

- for KamAZ vehicle:

400 l. With. × 85 rub./l. p.-13,200 = 20,800 rub.,

13,200 is the amount of tax deduction in the amount of the payment made for damage caused to roads.

The total amount of transport tax for 2018 is:

13,694 + 20,800 = 34,494 rubles.

Law of the Moscow Region dated November 16, 2002 No. 129/2002-OZ provides for the payment of advance tax payments.

The down payment for an entire quarter of ownership of the Audi A6 Avant quattro is:

13,694 / 4 = 3,424 rubles.

For the first and second quarters, advance payments are not paid, since the car was purchased only on August 27, 2018.

In the third quarter of 2018, the ownership coefficient is 0.3333 (Q = 1 month / 3 months). The advance payment, taking into account the ownership coefficient for the third quarter, will be: 3,424 × 0.3333 = 1,141 rubles.

The organization does not make advance payments for a KamAZ vehicle, since its maximum weight is over 12 tons (clause 2 of Article 363 of the Tax Code).

See how the transport tax return for 2018 should be filled out in the example considered:

Control ratios will help you independently detect errors associated with filling out a transport tax return.

Results

For 2017-2018, for reporting, use the new tax return form for transport tax, approved by Order of the Ministry of Finance of Russia dated December 5, 2016 No. ММВ-7-21/668@.

When filing a transport tax return for 2018, fill out lines 280 and 290 if you transferred payment for heavy goods. If you did not make heavy payments in 2018, cross out all the spaces on these lines. Line 070 “Date of vehicle registration” is required to be filled in by all taxpayers.

There is no need to put a stamp on the declaration, but the data on transport located in one subject of the Russian Federation can be combined.