Invoice for internal movement. Transfer of goods and materials within the enterprise. When is the document issued?

Accounting statements, accounting → Invoice for internal movement of materials. Form No. m-13

3 approved by order of the Central Administration of the USSR dated December 14, 1972 no. 816 +-+ enterprise, organization code 0303010 2 +-+ +-+ invoice no. +-+ on internal moving materials"" 20g. +-+ view object-object-operations -sender -receiver...

Accounting statements, accounting → Invoice for internal movement of materials. Form No. m-12

12 - approved by order of the Central Administration of the USSR dated 12/14/72 no. 816 +-+ enterprise, organization code 0303009 4 +-+ +-+ invoice no. +-+ on internal moving materials"" 20 +-+ corresponding workshop, facility, workshop, facility, ru...

Accounting statements, accounting → Sample. Invoice is a requirement for release (internal movement) of materials. Form No. m-11

Approved by the resolution of the State Statistics Committee of the USSR dated December 28, 1989 no. 241 +-+ (enterprise, organization) okud code +-+ invoice- requirement for leave ( internal moving) materials+-+ date number sos- code of delivery +- ment type...

Enterprise records management documents → Invoice for internal movement, transfer of goods, containers (Unified form N TORG-13)

Document " invoice on internal moving, transfer of goods, containers (unified form n bargaining-13)" in excel format you can receive...

Enterprise records management documents → Invoice for internal movement of fixed assets (Unified Form N OS-2)

Document " invoice on internal moving fixed assets (unified form n os-2)" in excel format you can get...

Accounting and financial documents → Certificate (invoice) of acceptance and transfer (internal movement) of fixed assets (form No. os-1, approved by Decree of the USSR State Statistics Committee dated December 28, 1989 No. 241)

89 n 241 +-+ Okud code +-+ approved by the head of the enterprise - - signature acting, last name "-" - 19th Act ( invoice) acceptance and transfer ( internal +-+ movements) fixed assets number date person code, document type code - composition responsible...

Accounting statements, accounting → Invoice for the release of materials to the third party. Form No. m-14

Ma no. M-14 approved by the Central Administration of the USSR on December 14, 1972, no. 816 +-+ okud code 0303011 9 (enterprise, organization) +-+ +-+ invoice no. +-+ for vacation materials on the side "" 20g. +-+ correspondent account code type of transaction warehouse +- (number...

Accounting statements, accounting → Invoice for the release of materials to the third party. Form No. m-15

Corresponding account +- type of operation warehouse account code analytic- sub-account. accounting +-+-+-+-+-+- +-+ invoice no. on vacation materials to the side "" 20 year basis to whom through whom +-+ nomen- one. quantity priceamountby...

Documents of the enterprise's office work → Invoice for the release of materials to the third party (Standard interindustry form N M-15)

Document " invoice on vacation materials on the side (standard interindustry form n m-15)" in excel format you can get from the link "...

Accounting statements, accounting → Sample. List of requirements for materials and calculation of the cost of materials for the object and sections of the estimate (form No. 4-mat)

Appendix 5 to the letter of the State Construction Committee of the Russian Federation dated 06/04/93 no. 12-146 form no. 4-mat statement of requirements for materials and cost calculation materials by object and sections of the estimate +-+ no. codes mathematical name materials scientist. if-cost...

Enterprise records → Consignment note

Document "transport" invoice" in excel format you can get it from the link "download file"

An invoice for internal movement is the primary accounting document for documenting the movement of inventory items within a trade organization.

It is issued taking into account a number of requirements applied to primary documents. The organization has the right to expand them by changing the form of the invoice or establishing additional requirements for its execution.

What is it used for and in what cases does it need to be issued?

The invoice is used to document the transfer of marketable products and packaging between structural divisions, warehouses or materially responsible persons of one organization. This could be moving goods from warehouse to warehouse or from warehouse to store. An invoice for internal movement is issued on the basis of an oral or written order from the manager.

What data does it include?

To account for internal movement, an organization has the right to develop its own document form or use the unified TORG-13 form. If an organization develops its own document form, it must be approved by order of the enterprise and contain the following data:

- Name of the organization;

- Title of the document;

- information about the sender and recipient of goods and materials;

- information about the transferred goods (its name and quantity in physical and value terms).

Features of compilation

The document for the movement of inventory items within the organization is drawn up by the materially responsible person from whose warehouse the inventory items are released. Vacation without documentation is not permitted.

TORG-13 is drawn up in two copies, and one remains with the person who released the goods, and the second - with the person who accepted them. The executed documents serve as the basis for writing off inventory items from the materially responsible person releasing them, and the department that received the inventory items accepts them for accounting on the basis of the invoice.

Numbering is carried out according to the rules established in each specific enterprise. As a rule, each type of document has its own continuous numbering; for ease of recording, a letter prefix can be added to the document number.

When filling out documents, special attention must be paid to the columns where the names of the sender and recipient should be indicated. Errors in the names of issuing and receiving structural units lead to distortion of data in accounting and to discrepancies between the actual availability of inventory and materials and data in accounting.

Errors in the names of inventory items are not allowed., for better identification, it is recommended to keep records not only by name, but also using a code. If goods of the same name differ in grade, it is necessary to indicate the grade of the goods and materials being sold.

Some types of inventory items can be accounted for in different units of measurement (for example, in kilograms and linear meters). When releasing such goods, it is necessary to indicate the unit of measurement in which they were accepted for accounting. The responsible person cannot transfer goods from one unit of measurement to another, bringing all sold goods and materials into a single form.

Columns indicating the quantity of goods sold are required.. When transferring inventory items in packages, you must indicate the number of piece products in one package and the number of such packages. The weight of the goods is indicated not only net, but also gross, if the financially responsible person has such information.

Data on the price and cost of inventory items at accounting prices are also indicated. The columns indicating quantity and amount are summed up and a total is summed up. The quantity of commercial products in various units of measurement is summed up for the purpose of control checking the quantity of products supplied.

Without specifying data on the exact name and quantity of goods and containers, the invoice for internal movement is invalid.

TORG-13 is signed by financially responsible persons who released and accepted the goods and materials. Be sure to indicate the names of their positions and the transcript of the signature.

Without the signatures of financially responsible persons, the document is invalid. It is not allowed to endorse the invoice by a person who does not have the right to do so. The right to sign is assigned by order of the organization.

Without the signatures of financially responsible persons, the document is invalid. It is not allowed to endorse the invoice by a person who does not have the right to do so. The right to sign is assigned by order of the organization.

The unified form does not provide for the affixing of a seal, however, if materially responsible persons have seals in structural units, then in order to provide greater control and prevent forgery of signatures, it is recommended to affix them additionally. The absence of a seal is not a violation unless it is established by a local act of the organization.

Is it necessary to record the document in the accounting journal?

Documents reflecting the movement of inventory items within the enterprise are recorded in the accounting journal. A record of an invoice for internal movement is reflected for both the issuing and receiving parties.

The form of the journal can be arbitrary, but it must contain data that allows you to identify the documents specified in it:

- document number and date of issue;

- name of the unit - the second party to the business transaction for the movement of inventory items;

- the total quantity and amount of inventory items indicated in the invoice.

The materially responsible person reflects data on the movement of inventory items in warehouse accounting cards, and they themselves invoices are transferred to the accounting department of the enterprise according to the register.

How long should it be stored?

All primary documents must be stored in the organization for five years after the reporting year, i.e. the year in which they were issued, then they can be destroyed.

They may be needed if discrepancies are identified during a warehouse inventory or to confirm the correctness of the reflected data during a tax audit.

Thus, the internal movement of goods and containers is documented with an invoice. The organization has the right to develop its own document form or use the unified TORG-13 form. It is stored in the company's accounting department for five years, after which it can be disposed of.

If you find an error, please highlight a piece of text and click Ctrl+Enter.

In the process of economic activity, material assets arrive at warehouses and storerooms not only from suppliers. Their internal movement is also carried out from the organization’s departments to storerooms and warehouses. Paragraph 57 of Methodological Instructions No. 119n establishes that the delivery of materials to warehouses by departments must be documented with invoices for the internal movement of materials in cases where:

products manufactured by divisions of the organization are used for internal consumption in the organization or for further processing;

the organization's divisions return materials to the warehouse or workshop storeroom;

waste from production of products (performance of work), as well as defects are handed over;

delivery of materials received from the liquidation (disassembly) of fixed assets is carried out;

other similar cases.

Operations for the transfer of materials from one division of the organization to another are also documented with invoices for the internal movement of materials.

Resolution No. 71a for these purposes developed form No. M-11 “Demand-invoice”, used in cases where material assets are moved between structural divisions of an organization or between financially responsible persons.

The invoice is drawn up by the financially responsible person of the structural unit that delivers the material assets. One of the two compiled copies of the invoice serves as the basis for the delivering warehouse to write off valuables; on the basis of the second copy, the receiving warehouse accepts these values for accounting. The invoice is signed by the financially responsible persons of both the delivering and receiving departments and is submitted to the accounting department to record the movement of materials.

It should be noted that the same invoices are used to document the delivery of on-demand and unused materials to the warehouse, as well as the delivery of waste and defects.

The internal movement of materials is also considered as their release to warehouses (storerooms) of the organization's divisions and to construction sites.

In the case when the release of materials to departments is carried out without indicating the purpose of use of the materials, such release is also taken into account as an internal movement, and the materials are considered to be issued to the department that received them. The department that received the materials draws up a consumption report for the amount of materials actually consumed. The specific procedure for drawing up an expense report, as well as the list of departments that can apply it, are established by the organization. This act must reflect:

name of the received materials;

quantity, accounting price and amount for each item;

number and (or) name of the order, product, product for the production of which the materials were used;

quantity of manufactured products or volumes of work performed.

The drawn up act is the basis for writing off materials from the reporting unit of the unit that received them.

In case of movement of inventory items between structural divisions or materially responsible persons of the organization, in accordance with Resolution No. 132, an Invoice for internal movement, transfer of goods, containers (form No. TORG-13), drawn up in two copies by the materially responsible person of the warehouse or division, is drawn up. handing over inventory items. The first copy of the invoice remains in the delivery department and serves to write off inventory items, the second is transferred to the department receiving the values and serves to accept them for accounting.

The invoice is signed by the financially responsible persons of the deliverer and recipient and submitted to the organization’s accounting department to record the movement of inventory items.

Within an organization, not only materials and goods, but also fixed assets are moved from one structural unit to another. To register and record such movements, the Invoice for internal movement of fixed assets, form No. OS-2, is used.

The invoice is issued by the transferring unit in triplicate and signed by the responsible persons of the structural units of the recipient and the deliverer. The first copy is transferred to the accounting department, the second remains with the financially responsible person of the division transferring the fixed asset, and the third copy is transferred to the division receiving the fixed asset.

Data on the movement of fixed assets is entered into the inventory card or book of accounting of fixed assets (forms No. OS-6, No. OS-6a, No. OS-6b).

In the process of moving property, which is part of fixed assets, between divisions of one company, an invoice is drawn up in the OS-2 form. For each transferred property, the form must be filled out separately. The employee who is a direct participant in the process of transferring the object is responsible for issuing the invoice.

The document must be completed in triplicate. The first remains with the materially responsible person (MRP) carrying out the transfer. This copy must be signed by the entity accepting the property.

Dear readers! The article talks about typical ways to resolve legal issues, but each case is individual. If you want to know how solve exactly your problem- contact a consultant:

It's fast and FOR FREE!

The receiving party retains a second copy of the invoice with the signature of the transmitter. The third copy must contain the signature of both parties and is transferred to the accounting department by the employee who enters the necessary data for the OS-6 inventory card.

Main details of the procedure

Purpose and standards of the document

The invoice for the internal movement of objects confirms the fact of the transfer of property, which allows for the write-off and receipt of valuables. The basis is the content in the document of complete information about the participants in the fact of transfer and the parameters of the object.

The essential details that any invoice contains include:

- a list of all parties participating in the procedure;

- type of transferred object and its characteristics;

- quantity and price of transferred property;

- signatures and list of all responsible persons;

- related documentation.

Depending on the type of operation being carried out, it is possible to enter additional details without changing or excluding the required ones. It is allowed to use unified forms of documents that were approved by Decree of the State Statistics Committee No. 132 or independently developed templates with the preservation of mandatory information

Federal Law No. 402 defines the mandatory details that must be present in the primary document. In case of non-compliance with this norm, the document will be refused acceptance for registration.

Methodological recommendations adopted by Roskomtorg Letter No. 1-794/32-5 dated July 10, 1996 confirm the need to document the movement of property with shipping documentation. The invoice is drawn up by the financially responsible person during the transfer process.

Shape characteristics

Depending on the property being transferred, unified forms such as TORG-13 and OS-2 can be used. TORG-13 is applied in case of transfer of goods or materials to a company. OS-2 is used when the movement of fixed assets is required. Unlike OS-2, the TORG-13 invoice requires only two copies and does not need to be filled out in a strict form.

The document is valid if transferred by any MOL or department. The form is a guarantor of the movement of goods to another entity. Most often, such a document is completed before or during the transfer.

Invoice form for internal movement of objects:

Sample filling

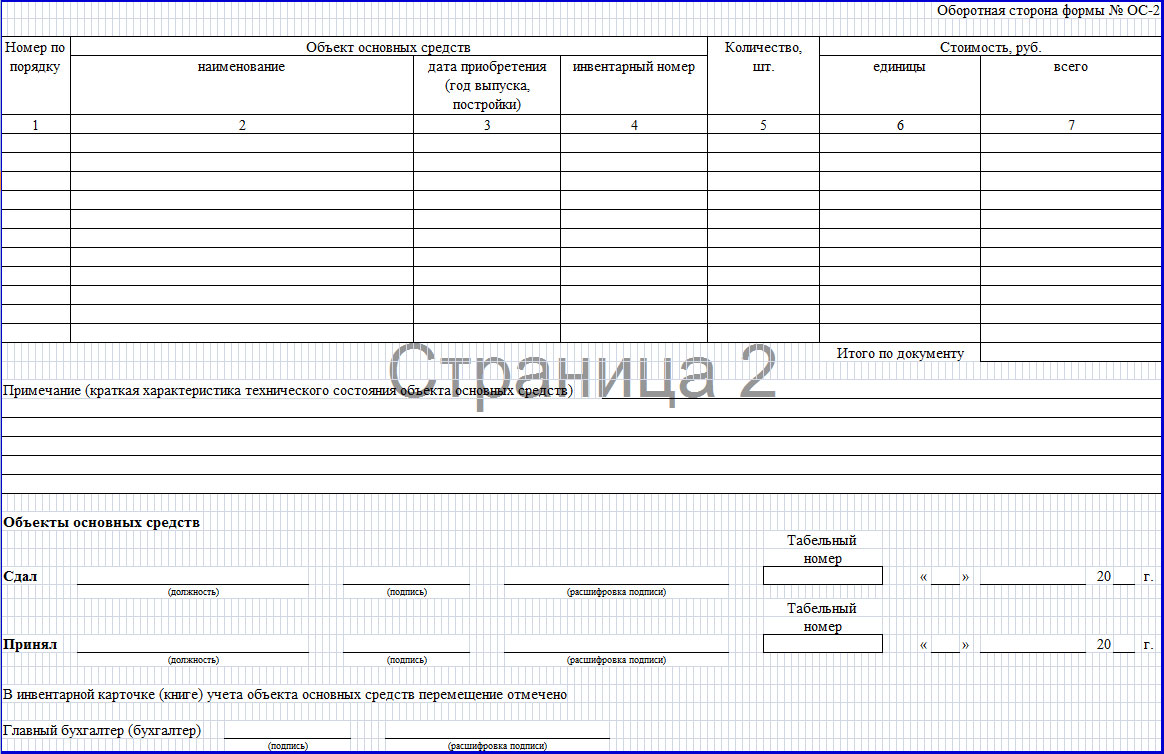

The invoice for the internal movement of objects OS-2 is drawn up in triplicate. The first goes to the entity performing the registration of the movement, the second goes to the recipient, and the third goes to the accounting department. The header located on the front side of the document is filled with information, including the name of the company, the deliverer and the receiver, OKUD codes and, the date when the filling took place and the serial number are also entered.

In the main part of the OS-2 act there is a table containing the following points:

- OS number;

- name of the property;

- transfer date;

- inventory number;

- number of transferred objects;

- price of one unit;

- total cost.

Below the table there are lines where technical information about the condition of the transferred property is recorded. Afterwards, the signatures of the parties, their transcript, the position of each of the MOLs, the report card number and date are located. Form OS-2 must be signed by the chief accountant.

Tips for maintaining an invoice for internal movement of objects

A transfer within an organization is not considered a sale because there is no transfer of ownership. Both independent development and approval of the document and the use of a unified form are allowed.

In the case where the division is not allocated to a separate balance sheet, the use of the OS-2 form is allowed. Otherwise, this form will not be enough, so it is better to develop and approve your own form.

Information about the fact of moving objects must be included in the OS-6 inventory jacket of the transferred OS (if a unified form is used).

If the OP is allocated to a separate balance sheet, together with the invoice, the recipient must receive the following documents:

- in accordance with the OS-1 form, issued at the time of admission;

- a complete set of technical documentation.

Reflection of the fact of transfer of an object in accounting is carried out depending on the allocation of the EP to a separate balance sheet. If the division is allocated to a separate balance sheet, then the movement is reflected using the “intra-business settlements” account (sub-account “Settlements for allocated property”).

In cases where a division is not allocated to a separate balance sheet, analytical accounting is maintained using the “Fixed Assets” account. If such analytics are not carried out, then it is permissible not to enter the movement into accounting.

Expenses that arose in the process of moving property in accounting are classified as production costs of the department. To calculate income tax, expenses that were associated with the movement of property are usually classified as other expenses and confirmed by a certificate of work performed.

If the moving work was carried out in-house, then an accounting certificate is drawn up with invoices attached for the materials used, payroll statements, waybills, etc. Input VAT on work that was performed by third-party companies must be deducted based on the invoice - textures.

Sample of filling out an invoice for internal movement of objects:

Reflection of actions on paper

How to take into account the movement of an object depends on the presence of a separate balance sheet for a separate unit.

In the case where the division is on the general balance sheet, the following transactions must be made: D01, subaccount OP-2 - K01, subaccount OP-1 - fixed assets are moved from the transferring division to the receiving one. Then, they move: D02, subaccount OP-1 – K02, subaccount OP-2.

In the case where the division is on a separate one, the following transactions should be made: D79, subaccount 1 - K01 - the initial cost of the moved object is written off. Afterwards, the accumulated depreciation savings are transferred: D02 - K79, subaccount 1.

The second division receives fixed assets from the transferor: D01 - K79, subaccount 1, as well as accumulated depreciation: D79, subaccount 1 - K02. In this case, the initial cost of the object does not change. For this reason, depreciation on the received property of the unit that receives the object is calculated in accordance with the previous procedure.

Registration procedure

Form TORG-13 is filled out as follows. The header must include information about the company within which the move is being made. In addition, it is necessary to indicate the date when the invoice was drawn up and its number. Next, a table is filled in, the upper part of which is intended for information about the entity transferring the property and the recipient.

The table contains the following data on the transferred goods:

- number of objects;

- units;

- accounting value (established independently by the organization);

- the total value of the transferred property.

You can find a form and sample for filling out this document on the Internet. Upon completion of filling out, the signatures of the parties must be affixed.

Form OS-2 is filled out on both sides. The front side contains information about the legal entity with the full name of the divisions between which the object is transferred. The document also indicates the date of transmission and the serial number of the form. Afterwards, the table indicates the list of transferred property, date of manufacture or release, inventory number, number of transferred objects and their cost.

Examples of non-financial assignments

An invoice for the internal movement of an object constituting non-financial assets is used when registering and accounting for the movement between structural divisions of an institution of such objects as fixed assets, intangible assets, finished products produced by the enterprise.

Previously, a form was used that related only to fixed assets, but the instructions prescribed it for intangible assets and legal acts. Now even from the name it follows that the invoice is intended for all types of non-fiscal assets, despite the fact that the header only talks about fixed assets.

The composition of the indicators has undergone almost no changes: only details have been added that are associated with an increase in the scope of use of the form. “Base (type of document, date and number)” was added to the header. The table has been updated with units of measurement, which is directly related to the change in the purpose of the form.

Instructions for adding

To add an invoice for internal movement of property, you need to enter the context menu and click on add. The document parameters are indicated in the window that appears. The document type must be selected only when entering the first invoice into the system. In the future, this parameter will be selected automatically.

The data for automatically entering information into the “Organization” field is taken from the last invoice entered into the system for movement within the enterprise. The program will automatically assign a document number based on a unique sequence for a specific enterprise. The date of the document is set automatically.

The structural unit, as well as the Mol field, can be filled in automatically after entering the inventory property.

If the base document is not registered by the system, its details can be saved. To do this, fill in the required fields, after which you need to press the create button. This button is located next to the input fields.

If the base document is registered by the system, then the fields type, type, number and date of the document can be filled with information necessary for searching and further selection from the list of the base document. If there is only one document in the list that appears, it will be filled in automatically. The “Note” is filled with additional information.

After the basic parameters of the document have been filled in, detailed information about the object being moved is required. To do this, you need to open the “Invoice Specification” tab. Information can be added either as a list or individually.

To enter information about one of the objects, you need to select “Add” in the context menu. Next, the OS object is selected. After all fields have been filled in, you need to click “OK”. You can close without saving changes by pressing the “Cancel” button.

To add a list of positions, select the add list item in the specification menu. You can select more than one position in the window that appears by holding down the ctrl button on the keyboard. After all fields have been filled in, click “OK”.

Once the invoice has been registered, it can be sent for printing. To do this, select the required print item in the application menu. After printing, the document is sent to the financially responsible persons for signature.

Afterwards the invoice is processed in accounting. To do this, select “Workout” in the application menu, then “Work out”. After indicating the actual date of property movement in the window that appears, you need to press the “OK” button.

Upon completion of the work, the corresponding entries are generated and entered into the inventory file.

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week.

Business transactions that are not documented in primary accounting documents are not accepted for accounting and are not subject to reflection in accounting registers.

Primary accounting documents are accepted for accounting if they are compiled in accordance with the form contained in the albums of unified forms of primary accounting documentation.

Developed and approved unified forms of primary accounting documentation in accordance with Decree of the Government of the Russian Federation of July 8, 1997 No. 835 “On primary accounting documents” must be used by all organizations, regardless of their organizational and legal form.

In accordance with the Resolution of the State Statistics Committee of the Russian Federation dated March 24, 1999 No. 20 “On approval of the procedure for using unified forms of primary accounting documentation” in unified forms of primary accounting documentation, except for forms for recording cash transactions approved by the State Committee on Statistics of the Russian Federation, organization, if necessary may provide additional details. At the same time, all details of the approved unified forms of primary accounting documentation remain unchanged, including code, form number, document name. Removing individual details from unified forms is not allowed.

Changes made must be documented in the relevant organizational and administrative document of the organization.

The formats of the forms indicated in the albums of unified forms of primary accounting documentation are recommended and can be changed in terms of expanding and narrowing columns and lines, including additional lines and loose sheets for ease of placement and processing of the necessary information.

To accounting as inventories, in accordance with paragraph 2 of the Accounting Regulations “Accounting for Inventories” PBU 5/01, approved by Order of the Ministry of Finance of the Russian Federation dated June 9, 2000 No. 44n “On approval of the accounting regulations “Accounting” inventories" PBU 5/01", the following are accepted:

· raw materials, materials, and other assets used in the production of products intended for sale (performance of work, provision of services);

· assets intended for sale (and goods);

· assets used for the management needs of the organization.

According to the Russian Encyclopedic Dictionary, raw materials are raw materials and materials that have previously been exposed to labor and are subject to further processing (for example, mined ore).

There are primary and secondary raw materials. Primary raw materials include the already mentioned mined ore, raw cotton, natural gas, and so on; secondary raw materials are finished products that have become unusable - scrap metal, waste paper, and others.

Materials are products that are consumed with changes in shape, composition, and condition in the manufacture of products, including materials involved in the assembly or production of goods for sale. The cost of materials is included in the cost of production.

According to paragraph 42 of the Guidelines for accounting of inventories, approved by Order of the Ministry of Finance of the Russian Federation dated December 28, 2001 No. 119n “On approval of guidelines for accounting of inventories” (hereinafter Guidelines No. 119n), materials are a type stocks. Materials include raw materials, basic and auxiliary materials, purchased semi-finished products and components, fuel, containers, spare parts, construction and other materials.

Semi-finished products of own production are products the production of which is completed in one or more workshops, but are subject to further processing in other workshops or at other enterprises.

Warehouse accounting data for inventories and operational accounting of movement in the organization's divisions must correspond to the accounting data for inventories. The above provision is one of the main requirements for accounting of inventories.

Materials from the supplier's warehouses or from the transport organization are received by an authorized person of the organization.

The right of a person to act as a trustee of an organization when receiving material assets from suppliers is formalized by issuing powers of attorney (forms No. M-2 and No. M-2a). Unified forms of primary accounting documents for accounting of materials were approved by the Resolution of the State Statistics Committee of the Russian Federation dated October 30, 1997 No. 71a “On approval of unified forms of primary accounting documentation for accounting of labor and its payment, fixed assets and intangible assets, materials, low-value and wearable items, work in capital construction" (hereinafter Resolution No. 71a).

The power of attorney is drawn up in the accounting department in one copy and issued to the recipient against signature.

Organizations in which the receipt of material assets by power of attorney is of a massive nature, use form No. M-2a and the issuance of these powers of attorney is recorded in the logbook of issued powers of attorney, which is pre-numbered and laced.

Powers of attorney are issued only to persons working in this organization; the issuance of powers of attorney to other persons is not permitted. The power of attorney issued must be completely completed and must contain a sample signature of the person in whose name it is issued. According to paragraph 5 of Article 185 of the Civil Code of the Russian Federation (hereinafter referred to as the Civil Code of the Russian Federation), a power of attorney on behalf of a legal entity is issued signed by its head or another person authorized to do so by the constituent documents, with the seal of this organization attached. If based on state or municipal property, a power of attorney to receive or issue money and other property assets issued on behalf of such a legal entity must also be signed by the chief (senior) accountant of this organization.

A power of attorney for transactions requiring a notarized form must be certified by a notary, except as otherwise provided by law.

As a rule, powers of attorney are issued for 10 - 15 days, but in the case of receipt of inventory items as scheduled payments, a power of attorney can be issued for a longer period. The validity period of a power of attorney in accordance with Article 186 of the Civil Code of the Russian Federation cannot exceed three years. If the term is not specified in the power of attorney, it remains valid for one year from the date of its execution. A power of attorney that does not indicate the date of its execution is void.

All material assets entering the organization must be promptly registered by the relevant warehouses.

In some cases, in the interests of production, it is advisable to send material assets directly to the relevant divisions of the organization, bypassing warehouses. However, such material assets are reflected in accounting as received at the warehouse and transferred to the workshop or site. In the primary receipt documents, a note is made that material assets were issued to departments in transit, that is, without delivery to a warehouse or storeroom. It should be noted that the list of materials that can be sent in transit to divisions and areas of the organization must be determined and formalized by order.

Material assets arriving at the organization's warehouse must be carefully checked in relation to their compliance with the range, quantity and quality specified in the supplier's documents.

We draw the attention of readers to the fact that materials must be taken into account in the appropriate units of measurement, by weight, volume, count, and so on. The accounting price is also established using the same units of measurement.

In practice, there are often cases when materials are received in one unit of measurement, for example, in tons, and are released from the warehouse in another unit of measurement, for example, in liters. In such a situation, the acceptance for accounting and release of materials must be reflected in primary documents, warehouse cards and accounting registers simultaneously in two units of measurement. In this case, first the quantity is recorded in the unit of measurement that is indicated in the supplier’s documents, and then in brackets - the quantity in the unit of measurement in which the materials will be released from the warehouse.

If the supplier's documents indicate a larger or smaller unit of measurement than is accepted in the organization, such materials are accepted for accounting in the unit of measurement that is accepted in the organization.

Paragraph 50 of Methodological Instructions No. 119n states that if it is difficult to reflect the movement of material in two units of measurement, then you can transfer the material to another unit of measurement by drawing up a transfer act. In the act of transfer to another unit of measurement, you must indicate the amount of material in the units of measurement specified in the supplier’s documents and in the unit of measurement in which the material will be released from the warehouse. At the same time, the accounting price of the material is determined in a new unit of measurement. In the warehouse accounting card, entries on the acceptance of materials for accounting are made in the supplier’s unit of measurement, as well as in the new unit of measurement, with a reference to the act.

Paragraph 49 of Methodological Instructions No. 119n establishes that the acceptance and accounting of incoming materials, provided there are no discrepancies between the supplier’s data and actual data, is formalized by the relevant warehouses by drawing up receipt orders (form No. M-4). Instead of issuing a receipt order, it is allowed to affix a stamp on the supplier’s document, the imprint of which contains the same details as the receipt order. In this case, fill in the details of the stamp and put the next number of the receipt order, such a stamp is equated to the receipt order.

Receipt orders are issued for the actual amount of incoming valuables. For bulk homogeneous cargo, such as ore, limestone, sand, crushed stone, coal and others, which arrive from the same supplier several times during one day, it is allowed to draw up receipt orders for the whole day. Each acceptance is recorded on the back of the receipt order. At the end of the day, the turnover is calculated and the total is entered into the receipt order.

If, when receiving material assets, it is established that the received materials do not correspond to their assortment, quantity and quality specified in the supplier’s documents, then the receipt order form No. M-4 is not drawn up. In such a situation, it is drawn up Certificate of acceptance of materials (form No. M-7). This act is also drawn up to formalize the acceptance of materials received without documents.

This act is the legal basis for filing a claim with the supplier or sender.

The act is drawn up by a commission, which must include a financially responsible person, a representative of the sender (supplier) or a representative of a disinterested organization.

The act is drawn up in two copies, one of which with the attached documents is transferred to the accounting department, and the other to the procurement or accounting department for sending a letter of claim to the supplier. If the organization has a legal department, then drawing up a letter of claim can be entrusted to this department.

Receipt orders and acts of acceptance of materials must be drawn up on the day of their receipt. In some cases, when individual batches of materials are in the process of technical acceptance or laboratory testing, the materials are accepted for safekeeping. In this case, the warehouse manager or storekeeper makes entries about such materials in a special book. Records in this book are kept with the division of materials: “Materials awaiting acceptance” and “Materials accepted for safekeeping.” In warehouses and storerooms, such materials must be stored separately and their consumption is not allowed until the results of acceptance are clarified.

Please note that materials purchased by accountable persons are also subject to delivery to the warehouse. Acceptance of such materials for accounting is carried out in the generally established manner on the basis of invoices and checks of retail trade organizations, receipts for the receipt order when purchasing materials for cash in other organizations, a procurement act when purchasing materials from the population, that is, on the basis of documents confirming the purchase. These documents must be attached to the advance report of the accountable person.

Accounting for the movement of materials in the warehouse for each grade, type and size is carried out in Materials accounting card (form No. M-17), filled in for each item number of the material. Entries in the card are kept by the financially responsible person on the basis of primary receipt and expenditure documents on the day of the transaction.

The basis for recording operations for the receipt of goods are the Unified forms of primary accounting documentation for recording trade operations, approved by Resolution of the State Statistics Committee of the Russian Federation of December 25, 1998 No. 132 (hereinafter referred to as Resolution No. 132).

According to clause 2.1.1 of the Methodological Recommendations for accounting and registration of operations for the receipt, storage and release of goods in trade organizations, approved by the Letter of Roskomtorg dated July 10, 1996 No. 1-794/32-5, the procedure and timing for the receipt of goods in terms of quantity, quality and completeness and its documentation are regulated by the current technical conditions, delivery conditions, purchase and sale agreements and instructions on the procedure for accepting consumer goods in terms of quantity, quality and completeness.

The transfer of goods to the buyer is formalized by shipping documents provided for by the terms of delivery and transportation of goods. These can be waybills, waybills, railway waybills, bills, invoices.

Goods purchased by a trade organization for resale may be delivered directly to its warehouse, or may be accepted by the trade organization outside its own warehouse.

If acceptance is carried out outside the buyer’s warehouse (at the supplier’s warehouse, at a railway station, pier, at the airport), then receipt of the goods is carried out by the financially responsible person of the trade organization by proxy, which confirms the right of the financially responsible person to receive the goods. The procedure for registering a power of attorney was discussed above.

Clause 2.1.5 of the Methodological Recommendations for accounting and registration of operations for the receipt, storage and release of goods in trade organizations, approved by the Letter of Roskomtorg dated July 10, 1996 No. 1-794/32-5, determines that the procedure for accepting goods and documenting acceptance depend, in particular:

ü from the place of acceptance;

ü on the nature of acceptance (quantity, quality, completeness);

ü on the degree of compliance of the supply agreement with the accompanying documents (presence or absence).

Acceptance of goods by quantity and quality involves checking the compliance of the actual availability of goods with the data contained in transport, accompanying and (or) payment documents, and when accepting by quality and completeness - the requirements for the quality of goods stipulated in the contract.

Receipt of goods is processed in different ways - depending on the proximity of the office to the location of the warehouse. If the supplier's warehouse and office are located in the same place, then paperwork and delivery of goods occur simultaneously. The document for the release of goods in this case is the invoice.

If the warehouse of the supplier company is remote from the office, then the representative of the trade organization (materially responsible person) is issued a document to receive the goods, according to which material assets will be released to him at the warehouse. If there is no goods in the warehouse in the required quantity, the recipient is issued a new document - an invoice, which indicates the actual quantity of goods supplied. IN the invoice is indicated :

ü number and date of discharge;

ü name of the supplier and buyer;

ü name and brief description of the product;

ü quantity of goods;

ü price and total cost of the goods (including VAT), value added tax must be indicated on a separate line.

The invoice must be issued in 4 copies, the first two remain with the supplier (in the warehouse and in the accounting department), the remaining two are transferred to the buyer (in the accounting department and the financially responsible person). The invoice must be certified by the seals of the supplier and recipient and the signatures of financially responsible persons (one released the goods, the other accepted).

If the goods are in undamaged containers, then acceptance can be carried out by the number of pieces, gross weight or by the number of trade units and markings on the container. If the actual presence of the goods in the container is not checked, then it is necessary to make a note about this in the accompanying document.

If the quantity and quality of the goods correspond to the data specified in the shipping documents, then the accompanying documents (invoice, waybill and other documents certifying the quantity or quality of goods received) are stamped by the purchasing organization, which confirms the compliance of the accepted goods with the data specified in accompanying documents. The financially responsible person who accepts the goods puts his signature on the shipping documents and certifies it with the round seal of the trade organization.

To formalize the acceptance of goods in terms of quality, quantity, weight and completeness in accordance with the rules for acceptance of goods and the terms of the contract, it is used Certificate of acceptance of goods (form No.TORG-1), with set by members of the selection committee authorized by the head of the organization. Goods are accepted based on actual availability.

The number of copies of the act to be drawn up and the completeness of the attached documents is determined in each specific case.

To formalize the acceptance of inventory items that have quantitative and qualitative discrepancies with the data in the supplier’s accompanying documents, the following documents are used:

Act on the established discrepancy in quantity and quality when accepting inventory items (form No. TORG-2), drawn up for domestic goods in four copies;

- Act on the established discrepancy in quantity and quality when accepting imported goods (form No. TORG-3), compiled for imported goods in five copies.

Note!

If, at the time of acceptance of the goods, a discrepancy between the gross weight and the weight indicated in the accompanying documents is revealed, the buyer must not open the container and packaging. If, while the gross weight is correct, a shortage of goods is established during the check of the net weight or the number of commodity units in individual places, then the buyer has the right to suspend acceptance of the remaining cargo. The containers, packaging of opened items and the goods contained in them must be preserved and then handed over to a representative of the sender’s organization.

· Certificate of acceptance and transfer of fixed assets (except for buildings, structures) (form No. OS-1);

· Certificate of acceptance and transfer of groups of fixed assets (except for buildings, structures) (form No. OS-1b).

The acts are approved by the heads of the recipient organization and the donating organization and are drawn up in at least two copies. The act must be accompanied by technical documentation related to this fixed asset item.

Data on the acceptance of an object into fixed assets is the basis for filling out the following primary documents for accounting for fixed assets:

· Inventory card for accounting of fixed assets (form No. OS-6);

· Inventory card for group accounting of fixed assets (form No. OS-6a);

· Inventory book for accounting of fixed assets (form No. OS-6b).

In the process of economic activity, material assets arrive at warehouses and storerooms not only from suppliers. Their internal movement is also carried out from the organization’s departments to storerooms and warehouses. Paragraph 57 of Methodological Instructions No. 119n establishes that that delivery of materials to warehouses by departments should be documented with invoices for internal movement of materials in cases where:

· products manufactured by divisions of the organization are used for internal consumption in the organization or for further processing;

· materials are returned by departments of the organization to a warehouse or workshop storeroom;

· waste from production of products (performance of work), as well as defects are handed over;

· delivery of materials received from the liquidation (disassembly) of fixed assets is carried out;

· other similar cases.

Operations for the transfer of materials from one division of the organization to another are also documented with invoices for the internal movement of materials.

Resolution No. 71a developed for these purposes form No. M-11 “Demand-invoice” , used in cases where material assets are moved between structural divisions of an organization or between financially responsible persons.

The invoice is drawn up by the financially responsible person of the structural unit that delivers the material assets. One of the two compiled copies of the invoice serves as the basis for the delivering warehouse to write off valuables; on the basis of the second copy, the receiving warehouse accepts these values for accounting. The invoice is signed by the financially responsible persons of both the delivering and receiving departments and is submitted to the accounting department to record the movement of materials.

It should be noted that the same invoices are used to document the delivery of on-demand and unused materials to the warehouse, as well as the delivery of waste and defects.

Paragraph 90 of Methodological Instructions No. 119n defines that internal movement of materials is also considered as their release to warehouses (storerooms) of organizational units and to construction sites.

In the case when the release of materials to departments is carried out without indicating the purpose of use of the materials, such release is also taken into account as an internal movement, and the materials are considered to be issued to the department that received them. The department that received the materials draws up a consumption report for the amount of materials actually consumed. The specific procedure for drawing up an expense report, as well as the list of departments that can apply it, are established by the organization. This act must reflect:

ü name of the materials received;

ü quantity, accounting price and amount for each item;

ü number and (or) name of the order, product, product for the production of which the materials were used;

ü quantity of manufactured products or volumes of work performed.

The drawn up act is the basis for writing off materials from the reporting unit of the unit that received them.

In case of movement of inventory items between structural divisions or materially responsible persons of the organization in accordance with Resolution No. 132, Invoice for internal movement, transfer of goods, containers (form No.TORG-13) , drawn up in two copies by the financially responsible person of the warehouse or department handing over inventory. The first copy of the invoice remains in the delivery department and serves to write off inventory items, the second is transferred to the department receiving the values and serves to accept them for accounting.

The invoice is signed by the financially responsible persons of the deliverer and recipient and submitted to the organization’s accounting department to record the movement of inventory items.

Within an organization, not only materials and goods, but also fixed assets are moved from one structural unit to another. To register and record such movements, it is used Invoice for internal movement of fixed assets, form No. OS-2, approved by Resolution of the State Statistics Committee No. 7.

The invoice is issued by the transferring unit in triplicate and signed by the responsible persons of the structural units of the recipient and the deliverer. The first copy is transferred to the accounting department, the second remains with the financially responsible person of the division transferring the fixed asset, and the third copy is transferred to the division receiving the fixed asset.

Data on the movement of fixed assets is entered into the inventory card or book of accounting of fixed assets (forms No. OS-6, No. OS-6a, No. OS-6b).

Material assets can be released from the warehouse into production, as well as in the event of their sale and disposal for other reasons.

Release of material into production is the issuance of materials from a warehouse or storeroom directly for the manufacture of products, performance of work and provision of services, as well as for the management needs of the organization.

Depending on how the warehouse structure is organized, materials are released in accordance with established standards and in appropriate units of measurement as follows:

ü either to the warehouses of the organization’s divisions and from there directly to production - to sites, to teams and to workplaces;

ü or directly to departments if they do not have warehouses.

Please note that storekeepers release materials from the warehouse to strictly defined employees. Lists of persons who have the right to receive materials from warehouses, as well as samples of their signatures, must be agreed upon with the chief accountant of the organization and brought to the attention of financially responsible persons who issue materials.

The procedure for releasing materials into production from department warehouses directly to sites, teams and workplaces is carried out in the manner established by the head of the department.

Let's consider what primary documents are used to document the release of materials from the warehouse.

We noted above that the issuance of materials is carried out in accordance with established standards, that is, the release of materials into production must be carried out on the basis of pre-established limits. Such limits are established on the basis of material consumption standards and production programs developed in the organization.

To register the release of materials according to approved limits, it is used Limit-fence card (form No. M-8). This document is also used for ongoing monitoring of compliance with established limits for the supply of materials, and is also a supporting document for writing off material assets from the warehouse. The issuance of the limit-fence card is carried out by the divisions of the organization that are entrusted with the functions of supply or planning.

For each name of material, two copies of the document are issued, one of which is transferred to the structural unit before the beginning of the month, and the other to the warehouse. As a rule, a limit card is issued for a month, but if the movement of materials in an organization is small, then this document can be issued for a quarter. A separate limit and withdrawal card is issued for each warehouse.

When issuing materials, the storekeeper notes in both copies of the document the date and quantity of materials issued and displays the remainder of the limit according to the item number of the material. The warehouseman signs the recipient's limit and intake card, and the recipient signs the warehouse's limit and intake card.

After using the limit, the warehouse manager or storekeeper hands over the limit cards to the accounting department. Regardless of whether the limit is used or not, at the beginning of the month all limit cards for the previous month must be turned in. If the card was issued for a quarter, it must be returned at the beginning of the next quarter. The delivery of warehouse copies of limit-fence cards is preceded by reconciliation of the data contained in them with the data of copies of cards held by recipients of material assets. The completed reconciliation is confirmed by the signatures of the warehouse manager (storekeeper) and the responsible person of the department that received the materials.

To reduce the number of primary documents, it is recommended to issue materials in Material accounting cards (form No. M-17). In this case, the limit intake card is issued in one copy and on its basis the operation of releasing materials is carried out. The storekeeper signs the limit-fence card, and the recipient of the materials signs the materials accounting card.

When registering the issue of materials without registering consumable documents, warehouse cards are submitted to the accounting department according to the register at the end of each month. Based on the cards, accounting employees compile the appropriate accounting registers, after which the warehouse accounting cards are returned to the warehouse.

Accounting for the return of materials not used in production is kept in the same form, and no additional documents are drawn up.

If necessary, with the permission of the head of the organization, chief engineer or other authorized persons, excess supply of materials is allowed, as well as the replacement of some types of materials with others. If materials are issued in excess of the limit, the inscription “Above the limit” is written in the primary documents.

As a rule, large organizations carry out centralized delivery of materials from the organization's warehouses to the warehouses of the divisions and directly to the sites and workplaces of the divisions. In this case, a special operational document for vacation is drawn up - a “plan-map”. It reflects the established limits and calendar dates for submitting materials to departments. The plan-map form is not provided for in the albums of unified forms of primary accounting documents and must be developed by the organization independently. Based on this document, the warehouse employee issues an invoice for the release of materials within the established limit. In this case, the Requirement may be applied - invoice (form No. M-11), Invoice (form No. M-15).

All primary accounting documents for the release of materials from warehouses and storerooms to organizational units must indicate:

ü name of the material;

ü quantity of material, its price and total amount;

ü purpose of the material (name of the order, product, product for the manufacture of which materials are supplied, or name of the costs).

The release of materials from the organization's warehouse in the event of their sale is carried out by warehouse workers on the basis Invoice for the release of materials to the side (form No. M-15). This form is used to record the release of material assets:

ü to third parties on the basis of contracts and other documents;

ü farms of your organization located outside its territory.

The first copy of the invoice is transferred to the warehouse for the release of materials, and the second copy is transferred to the recipient of the materials.

The main document used to formalize the sale (release) of inventory items by a trade organization to a third party organization is Consignment note (form No.TORG-12), approved by Resolution No. 132 and drawn up in two copies. The first remains in the organization handing over inventory, and on its basis they are written off. The second copy is transferred to a third party and is the basis for accepting inventory items for accounting.

When transporting goods by road, a Consignment Note (Form No. 1-T) is issued, approved by Resolution of the State Statistics Committee of the Russian Federation of November 28, 1997 No. 78 “On approval of unified forms of primary accounting documentation for recording the work of construction machinery and mechanisms, work in road transport” .

The procedure for issuing a consignment note was established by the joint Instruction of the Ministry of Finance of the USSR No. 156, the State Bank of the USSR No. 30, the Central Statistical Office of the USSR No. 354/7 and the Ministry of Automobile Transport of the RSFSR No. 10/998 of November 30, 1983 “On the procedure for payments for the transportation of goods by road.”

According to paragraph 5 of this Instruction, the shipper does not have the right to transfer, and the motor transport organization does not have the right to accept for transportation, cargo that is not documented with waybills. This applies to all transportation performed by freight vehicles, regardless of the terms of payment for its work.

It should be remembered that the consignment note, in accordance with paragraph 6 of the Instructions, is the only document used for writing off inventory from shippers and accepting them for accounting from consignees, as well as for warehouse, operational and accounting.

The consignment note (hereinafter referred to as the CTN) is drawn up in four copies, but by agreement of the motor transport organization and the shipper it can be drawn up in five copies. Each copy of the TTN must be certified by the signature, seal or stamp of the shipper.

ü name of the recipient of the cargo;

ü name of the cargo;

ü quantity, weight of the cargo transported, method of determining the weight;

ü type of packaging;

ü method of loading and unloading;

ü time of delivery of the vehicle for loading and time of completion of loading.

In cases where it is not possible to list all the names and characteristics of the released inventory items in the TTN “Cargo Information”, an invoice in the form No. TORG-12 should be attached to it.

In these cases, the consignment note indicates that a specialized form is attached as a product section, without which this consignment note is considered invalid and should not be used for settlements with shippers and consignees, as well as for accounting for completed transportation volumes and calculating wages to the driver.

If one vehicle transports cargo to several recipients, then the TTN is issued for each shipment of cargo to each recipient separately.

As a rule, the consignment note is drawn up by the shipper, but the agreement may provide for the registration of the consignment note by the motor transport organization carrying out the transportation of goods.

If the consignment note is issued by the consignor, then motor transport enterprises have the right to check the information specified in the consignment note, and the consignor and consignee are responsible for the consequences of incorrect, inaccurate and incomplete reflection of information in the consignment note.

Acceptance of cargo for transportation is confirmed by the signature of the driver-forwarding agent in all copies of the consignment note, while the shipper has no right to demand that the driver accept the cargo using any other documents other than the consignment note.

The first copy remains with the shipper and is intended for writing off inventory items.

The second, third and fourth copies of the TTN are given to the driver, of which:

the second copy is handed over to the consignee and is intended for acceptance for accounting of inventory items;

the third copy is attached to the invoice for transportation and serves as the basis for the settlement of the motor transport enterprise with the shipper (consignee);

the fourth copy is attached to the waybill and serves as the basis for recording transport work.

When handing over the cargo, the driver presents three copies of the TTN to the consignee, who certifies the receipt of the cargo with his signature and seal (stamp) in the consignment note, simultaneously indicating in all copies the time of arrival and departure of the vehicle.

The consignment note consists of commodity and transport sections. The commodity section is used to write off inventory items from the shipper's warehouse and accept them for accounting by the consignee, the transport section is used to record transport work and make payments for services rendered for the transportation of goods.

More details with questions regardingorganization of warehouse accounting, You can find it in the book of JSC “BKR-Intercom-Audit” “Organization of warehouse accounting».